The first half of 2026 has further confirmed that AI is no longer simply a technology cycle – it is rapidly becoming the next layer of industrial infrastructure.

While global markets continue to navigate geopolitical uncertainty, slower consumer demand and shifting trade dynamics, investment momentum around AI, energy and computing infrastructure continues to accelerate. Across industries, the conversation has moved beyond experimentation and model development toward deployment, integration and execution at scale.

From a Venturous perspective, this transition represents one of the most significant structural shifts since the rise of cloud computing.

China Continues to Accelerate

Despite ongoing macro uncertainty and geopolitical tensions, China remains one of the most important markets shaping the next generation of industrial AI and smart infrastructure.

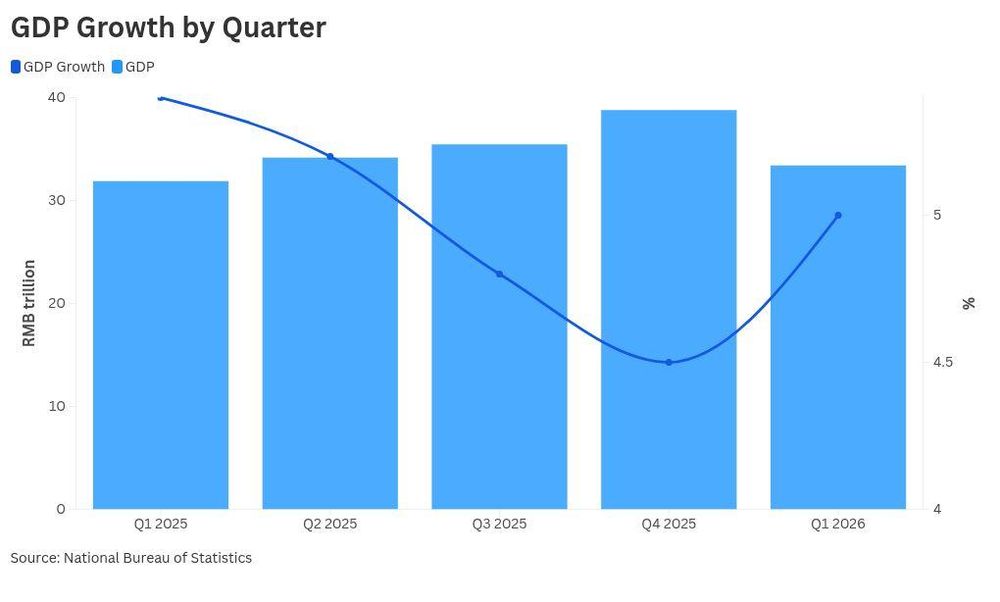

According to China’s National Bureau of Statistics, China’s GDP grew +5.0% YoY in Q1 2026, above market expectations. Industrial production increased +6.1%, while exports rose +14.7% to US$ 978 billion. Integrated circuits production grew +24.3%, highlighting the country’s continued focus on strategic technology and computing capacity. At the same time, retail sales increased only +2.4%, confirming that industrial expansion – rather than consumer growth – remains the primary driver of economic momentum.

This reflects a broader structural transition underway in China: from property-led growth toward advanced manufacturing, industrial AI, robotics and digital infrastructure.

AI is Moving From Generation to Execution

Over the past 18 months, global focus centred primarily around model development and generative AI capabilities. During the first half of 2026, however, value creation increasingly shifted toward deployment, enterprise integration and infrastructure enablement.

This includes:

- Enterprise AI Agents

- AI-powered industrial automation

- Smart buildings and energy optimisation

- AI infrastructure and compute capacity

- Physical AI and robotics

- Edge computing and distributed intelligence

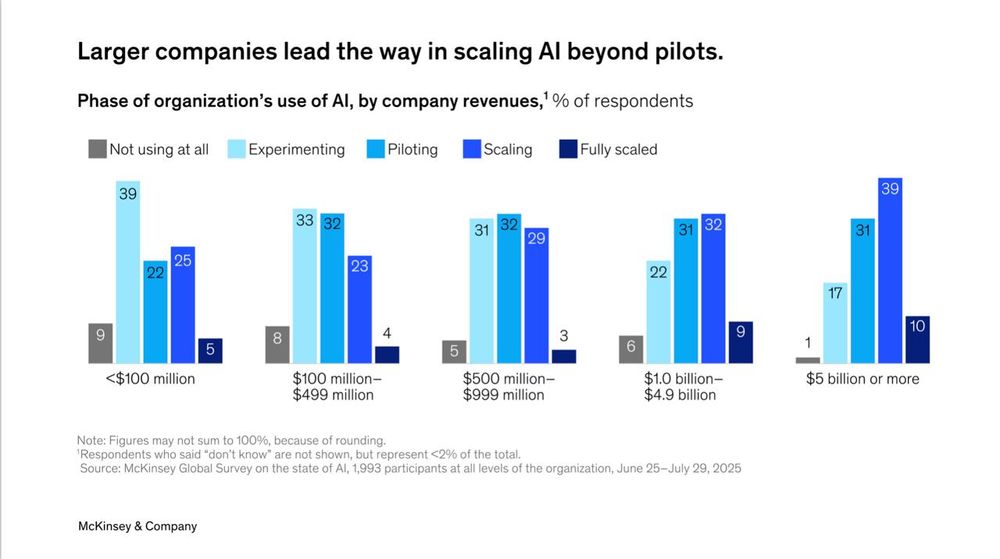

According to McKinsey, AI adoption among enterprises globally surpassed 72% in 2025, while Bloomberg Intelligence estimates the generative AI market could exceed US$ 1.3 trillion by 2032. At the same time, the International Energy Agency projects global electricity demand from data centres could more than double by 2030, driven largely by AI workloads.

As a result, compute supply, power infrastructure and deployment capability are increasingly becoming the strategic bottlenecks of the AI economy.

This is precisely where Venturous positions itself.

Venturous Ecosystem Momentum

During the first half of 2026, the Venturous ecosystem continued to build momentum across Smart Buildings, Smart Energy and Smart Computing.

Neuron Digital Group expanded its footprint to more than 827 connected buildings and recorded +106% YoY revenue growth in Q1 2026. SwanLink delivered +476% YoY revenue growth, driven by increasing adoption of OpenHarmony-based AIoT systems across industries including public security, mining and infrastructure.

Meanwhile, iSoftStone continued strengthening its position in enterprise AI and industrial automation. The company launched its “AI-First” ASDM platform, designed to transition enterprise software engineering from human-driven workflows toward AI-executed automation.

Across the broader ecosystem, Venturous now has influence over:

- 7.9 million+ AI-connected datapoints

- 10 billion+ kWh of energy coverage

- 827 buildings

- 60+ companies

- 94,000+ talents and ecosystem participants

Geopolitics and the US–China Relationship

The recent meeting between the US and China was closely monitored by global markets and technology investors.

Although strategic tensions remain high around semiconductors, AI leadership, supply chains and trade, the dialogue itself reinforced a growing reality: the economies of the United States and China remain deeply interconnected, particularly within AI infrastructure and advanced manufacturing.

Looking Ahead

Looking ahead, we believe the next phase of value creation will happen at the intersection of AI, energy, computing and physical infrastructure – as AI moves from generation to real-world execution at scale.

As we move into the second half of 2026, Therse are the themes which we believe will continue to define the market:

- The rise of Agentic AI and Physical AI

- Rapid expansion of AI infrastructure demand

- Growing importance of energy and compute availability

- Industrial deployment over consumer experimentation

- Continued convergence between software, hardware and real-world infrastructure

At Venturous, we continue to believe that the next phase of value creation will happen at the intersection of AI, energy, computing and physical infrastructure.

In many ways, 2026 may ultimately be remembered as the year AI moved from generation to execution.